How to Calculate Your Savings Rate? Step by Step With Real Examples

Let’s talk about something that sounds boring but is actually one of the most powerful numbers in your financial life: your savings rate. If you’ve ever wondered why some people seem to build wealth effortlessly while others struggle despite earning good incomes, the answer often comes down to this single metric. Your savings rate tells you exactly what percentage of your income you’re keeping versus spending, and trust me, once you start tracking it, you’ll never look at your finances the same way again.

The beauty of calculating your savings rate is that it’s surprisingly simple, yet it reveals so much about your financial health. It doesn’t matter if you’re earning $40,000 or $400,000, what matters is the gap between what comes in and what goes out. In this guide, we’ll walk through exactly how to calculate your savings rate using different methods, explore real-world examples, and help you understand what your number actually means for your financial future.

Understanding What Your Savings Rate Really Means

Before we dive into calculations, let’s get clear on what we’re actually measuring. Your savings rate is the percentage of your income that you save rather than spend. It’s that straightforward. But here’s where it gets interesting: this single percentage can predict how long it will take you to reach financial independence, how prepared you’ll be for emergencies, and whether you’re living within your means.

Think of your savings rate as your financial vital sign. Just like your doctor checks your blood pressure to assess your health, your savings rate tells you about your financial wellbeing. A healthy savings rate means you’re building a buffer against life’s uncertainties and creating options for your future. A low or negative savings rate means you’re walking a financial tightrope where one unexpected expense could throw everything off balance.

What makes the savings rate so powerful is that it’s completely under your control. You can’t always control how much you earn in the short term, but you have significant control over how much you save. This makes it an actionable metric rather than just another number to worry about.

The Basic Formula for Calculating Your Savings Rate

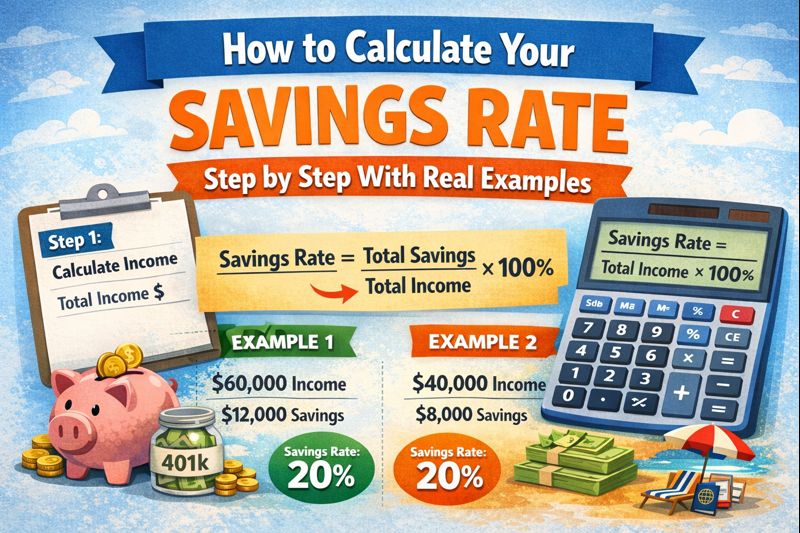

Let’s start with the simplest version of the savings rate calculation. The basic formula is:

Savings Rate = (Amount Saved / Gross Income) × 100

Here’s how this works in practice. Let’s say you earn $5,000 per month in gross income (before taxes). During that same month, you save $1,000 across all your savings vehicles, your 401(k), emergency fund, investment accounts, and any other savings. Your calculation would look like this:

Savings Rate = ($1,000 / $5,000) × 100 = 20%

This means you’re saving 20% of your gross income, which is actually quite solid. Many financial experts recommend saving at least 20% of your income, so you’d be right on target.

But here’s where things get a bit more nuanced. Some people prefer to calculate their savings rate based on net income (after-tax income) rather than gross income. This method can feel more realistic because you’re measuring what you save against what you actually take home. Using the same example, if your $5,000 gross income becomes $3,750 after taxes, your savings rate calculation changes:

Savings Rate = ($1,000 / $3,750) × 100 = 26.67%

Same savings amount, same income, but a different percentage. Neither method is wrong they just tell you different things. The gross income method is more conservative and comparable across different tax situations, while the net income method reflects your actual day-to-day financial reality.

What Counts as Savings? Breaking Down the Categories

Here’s where many people get confused: what exactly should you include in your “amount saved”? The answer is broader than you might think, and getting this right is crucial for an accurate savings rate.

Retirement Contributions

First and most obviously, all retirement contributions count as savings. This includes your 401(k) contributions, IRA contributions, and any employer match you receive. Yes, you should include the employer match even though it’s not technically your money yet, it’s still savings that’s building your net worth.

For example, if you contribute $500 to your 401(k) each month and your employer matches $250, that’s $750 total that goes into your savings calculation. Many people forget to include the employer match, which means they’re underestimating their actual savings rate.

Emergency Funds and Regular Savings Accounts

Any money you transfer into savings accounts, emergency funds, or money market accounts counts toward your savings rate. Even if you’re saving for a specific goal like a vacation or a down payment on a house, it’s still savings because you’re not spending it on current consumption.

Investment Accounts

Money that goes into taxable investment accounts, whether that’s a brokerage account, index funds, or individual stocks, definitely counts as savings. You’re setting aside money for future use rather than spending it now, which is the essence of saving.

Debt Repayment (With a Caveat)

This is where things get debatable. Some financial experts include extra debt payments (beyond minimum payments) in their savings rate calculation, particularly for mortgage principal or student loans. The logic is that paying down debt increases your net worth just like saving money does.

However, many prefer to keep debt repayment separate from savings rate calculations to keep things clear. There’s no universal rule here, but whatever you decide, be consistent in how you track it.

Real-World Examples Across Different Income Levels

Let’s look at three detailed examples that show how savings rates work across different life situations.

Example 1: The Entry-Level Professional

Sarah is 25 and just started her first job earning $50,000 per year ($4,167 per month gross). After taxes and health insurance, she takes home $3,000 per month. Here’s her monthly financial picture:

- Gross monthly income: $4,167

- 401(k) contribution: $200 (plus $100 employer match)

- Emergency fund transfer: $150

- Investment app: $50

- Total monthly savings: $500

Using the gross income method: ($500 / $4,167) × 100 = 12%

Sarah’s 12% savings rate is a good start for someone early in their career. She’s building the habit of paying herself first, and as her income grows, she can increase this percentage.

Example 2: The Mid-Career Couple

Michael and Jennifer are both 38, with a combined household income of $120,000 per year ($10,000 per month gross). After taxes, they take home about $7,200 monthly. Their savings breakdown:

- Combined 401(k) contributions: $1,000 (plus $500 employer match)

- 529 college savings for two kids: $400

- Roth IRA contributions: $500

- High-yield savings account: $300

- Total monthly savings: $2,700

Using the gross income method: ($2,700 / $10,000) × 100 = 27%

This couple has hit their stride with a 27% savings rate. They’re balancing current expenses with future needs, including retirement and their children’s education.

Example 3: The High Earner Playing Catch-Up

David is 45 and earns $200,000 per year ($16,667 per month gross). He started saving late but is now aggressive about it. After taxes, he takes home $10,500 monthly. His savings:

- Maxed-out 401(k): $1,958 (plus $500 employer match)

- Backdoor Roth IRA: $583

- Taxable brokerage account: $1,500

- Additional savings: $500

- Total monthly savings: $5,041

Using the gross income method: ($5,041 / $16,667) × 100 = 30.25%

David’s 30% savings rate shows that it’s never too late to get serious about saving. Despite starting late, his high savings rate means he can still build substantial wealth before retirement.

How to Improve Your Savings Rate Starting Today

Now that you know how to calculate your savings rate, let’s talk about improving it. The math is simple: increase income, decrease expenses, or ideally both. But the execution requires strategy.

Start by calculating your current baseline. Track one month of income and savings carefully to see where you stand. Don’t judge yourself, just get the number. Many people are surprised to discover they’re either saving more than they thought (encouraging!) or less than they realized (motivating!).

Next, set a realistic target. If you’re currently saving 5%, don’t immediately aim for 30%. Instead, try to increase by 1-2 percentage points each quarter. Small, consistent improvements compound over time. You might automate an extra $50 monthly to your 401(k) this quarter, then another $50 next quarter.

Focus on the big three expenses: housing, transportation, and food. These typically eat up 60-70% of most people’s budgets. Even small percentage reductions in these categories can dramatically improve your savings rate. Could you refinance your mortgage, keep your car an extra two years, or reduce dining out by one meal per week? These decisions create more breathing room in your budget.

What Your Savings Rate Says About Your Financial Timeline

Here’s the really exciting part: your savings rate doesn’t just tell you about today, it predicts your financial future with surprising accuracy. If you maintain a 50% savings rate, for instance, you can theoretically achieve financial independence in about 17 years. A 25% savings rate extends that timeline to about 32 years, while a 10% savings rate means you’re looking at approximately 51 years until you could retire.

This relationship exists because your savings rate reflects both how much you’re accumulating and how much you need to sustain your lifestyle. Someone who saves half their income only needs to accumulate enough to replace the other half. Someone who saves just 10% needs to accumulate enough to replace 90% of their income, a much bigger target.

Understanding this connection transforms your savings rate from a mere percentage into a powerful planning tool. Every percentage point increase accelerates your timeline to financial freedom. This is why seemingly small improvements in your savings rate can have outsized impacts on your long-term wealth building.

The bottom line? Your savings rate is the single most important number in personal finance. It’s simple to calculate, completely within your control, and directly connected to your financial future. Start tracking it today, and you’ll gain clarity about where you stand and what you need to do to reach your goals. The number might surprise you, challenge you, or encourage you—but it will definitely empower you to make better financial decisions going forward.